Why I Trade 200± NIFTY Straddles (And When to Flex with ATR/ADR)

Why I Trade 200± NIFTY Straddles (And When to Flex with ATR/ADR)

-

Why I Trade 200± NIFTY Straddles (And When to Flex with ATR/ADR) By Santanu Bez

By Santanu Bez

Have you ever wondered why I consistently trade 200± NIFTY straddles instead of ATM straddles?

Many traders ask me, curious why I use this structured approach when the market changes daily.

Here is a logic-driven, practical explanation that may transform your straddle trading perspective, especially if you seek systematic, low-stress, scalable intraday income using the D-SMART Contra method.

️ The Beauty of 200± Straddles

️ The Beauty of 200± Straddles Fixed strike distances (Spot+200 and Spot–200) give clear structure.

Fixed strike distances (Spot+200 and Spot–200) give clear structure.

No emotional confusion on where to position each day.

Clean Renko/PnF and premium ratio charts for analysis.

Manageable premium decay without ATM’s rapid stress.

Backtested and real trades confirm high hit rates for small, consistent targets.In a market of infinite uncertainty, fixed structure anchors your emotional and operational stability.

But What About Volatility?

But What About Volatility?Markets do not remain static.

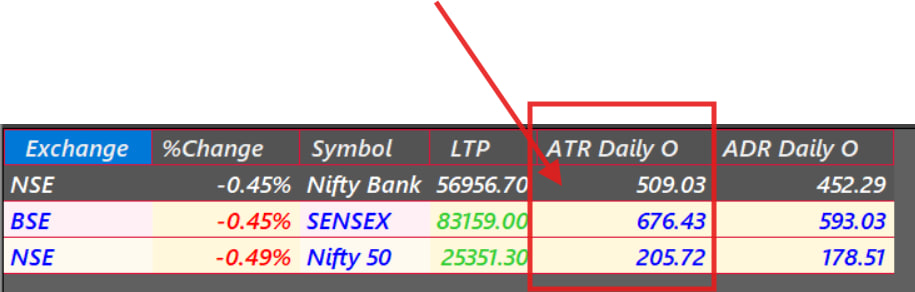

Daily ATR (Average True Range) and ADR (Average Daily Range) fluctuate, shifting premium behavior.

On low volatility days:

- 200± may feel too wide, with lower premiums.

On high volatility days:

- 200± may feel too tight, risking quick stop-outs.

Should you adjust daily with ATR/ADR flex?

Theoretically, yes.

Theoretically, yes.

Practically, frequent changes create:- Analysis overload.

- Inconsistent learning cycles.

- Emotional fatigue from constant recalibration.

The Best of Both Worlds: Anchored Flexibility My refined approach:

The Best of Both Worlds: Anchored Flexibility My refined approach:“Fixed 200± as the default, ATR/ADR-based adjustment only when volatility regime & value of underlaying shifts.”

🪄 How It Works:

Use 200± straddles daily by default under normal ATR/ADR conditions. If ATR/ADR changes ≥30% from your baseline (around 180–200 on NIFTY), adjust strikes:- ATR = 250 → 0.8 × 250 = 200 → Use 200–250±.

- ATR = 300 → 0.8 × 300 = 240 → Use 250±.

- ATR = 150 → 0.8 × 150 = 120 → Use 100–150± if premiums remain viable.

This aligns your strike distance with the market’s real movement potential while maintaining structured discipline.

Premium Sufficiency as a Filter

Premium Sufficiency as a FilterBefore executing any straddle:

Check combined premium:- If too low (₹30–₹50): Theta benefit isn’t worth it; consider ATM with tight SL or skip.

- If high due to events: Ensure strike adjustments align with acceptable risk.

Always trade only when premium justifies the trade.

ATR Bands: A Silent Guide

ATR Bands: A Silent GuideRather than recalculating daily, plot:

- 1 ATR above and below spot on your NIFTY chart.

If 200± strikes fall within the ATR band: alignment confirmed.

If ATR bands significantly exceed 200±: consider strike adjustment.This keeps volatility awareness while avoiding daily complexity.

Why This Approach Works Simplicity: Consistent, emotion-free execution.

Why This Approach Works Simplicity: Consistent, emotion-free execution.

Volatility Awareness: Adjust only when truly necessary.

Emotional Stability: Prevents over-analysis and stress.

Risk Consistency: Exposure aligns with volatility.

Scalability: Easy to replicate while scaling up.

️ Practical Comparison Table

️ Practical Comparison TableAspect Fixed 200± ATR/ADR Flex Simplicity Easy Complex

ComplexVolatility Matching Limited StrongEmotional Load Low HigherPremium Consistency Stable VariablePractical Returns Reliable Potentially higher in high ATR

️ Final Takeaway

️ Final Takeaway“Fixed 200± straddles as your core execution plan, with ATR/ADR flex only during meaningful volatility shifts, is the best of both worlds for systematic, low-stress, scalable straddle trading under the D-SMART Contra framework.”

This approach allows you to:

Respect market structure,

Harness theta decay,

Align with volatility context,

without sacrificing operational simplicity.

️ Disclaimer

️ DisclaimerThis article is for educational purposes only and reflects my personal trading approach and learning journey. Trading options carries risk. Always consider your risk tolerance, capital, and seek professional advice if needed. Past performance or personal strategy suitability does not guarantee future results. Trade responsibly.

Stay structured, let your discipline compound, and evolve with the market systematically.

Stay structured, let your discipline compound, and evolve with the market systematically.– Santanu Bez

-