Wrong enty exit and differences in Momentify Portfolio and RZone backtest

-

Hello Definedge team,

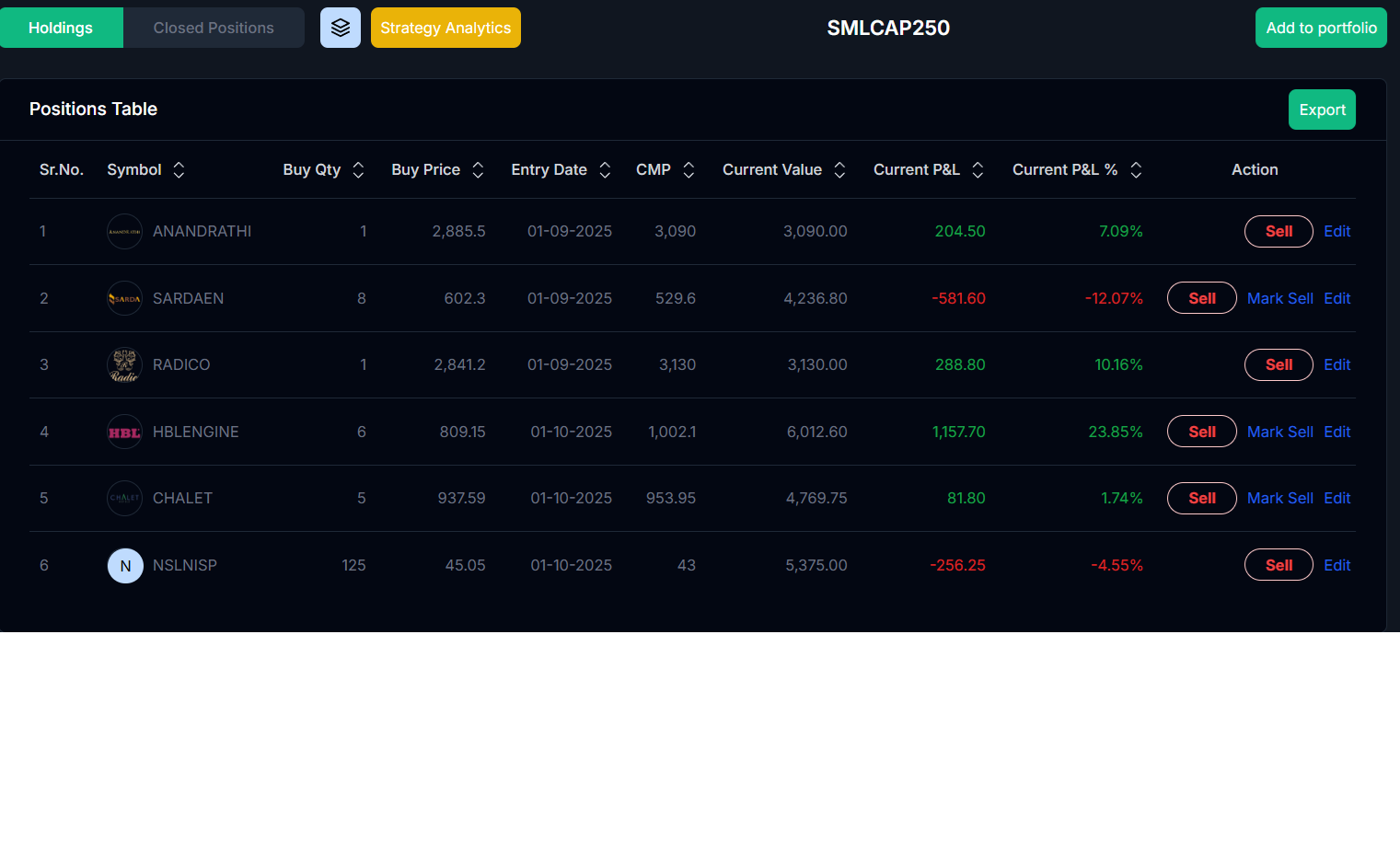

I made a portfolio and invested through Momentify (after doing backtesing for several days ) on 01-Sep-25, I got 17 shares as per scanner conditions and strategy (Allotted 1 lakh on 20 stocks, but got 17 as per stock selection criteria). On 1-Oct-25 , did rebalancing as per rules , the strategy squared off 14 stocks and gave entry to 3 new stocks, so I have total = 17 -14 +3 = 6 stocks on 31st-Oct-25. Now rebalancing date is on 01-Nov-25 (Saturday is off, will do on 03-Nov-25). I got a mail for rebalancing, I checked the basket so it is showing 3 outing stocks and 3 incoming as per strategy criteria. All is okay till here because we have to rely on Momentify and don't have to do the changes manually as advised by Mr Prashant ji and it's the core and important idea of investing through this method for long term.

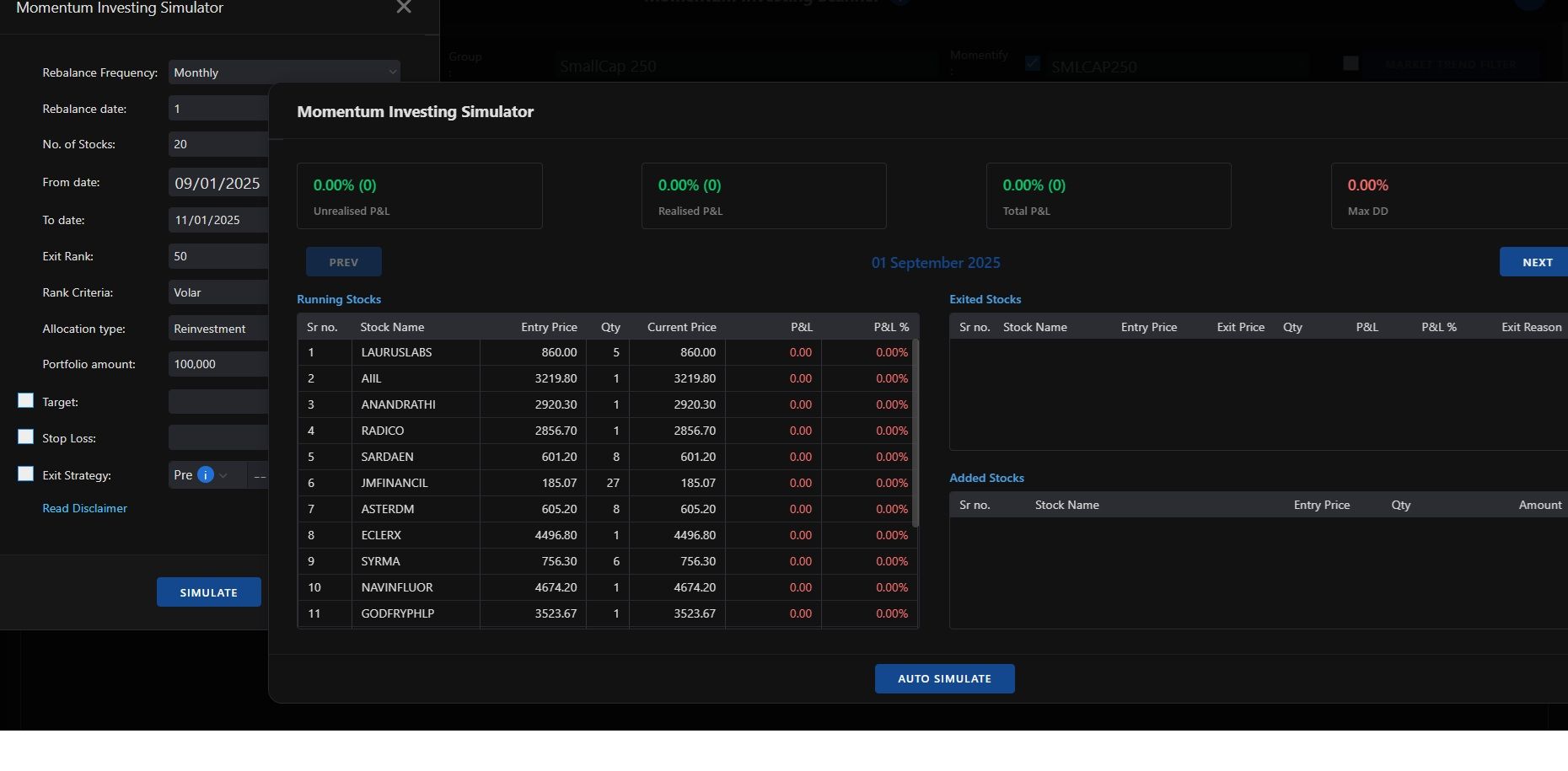

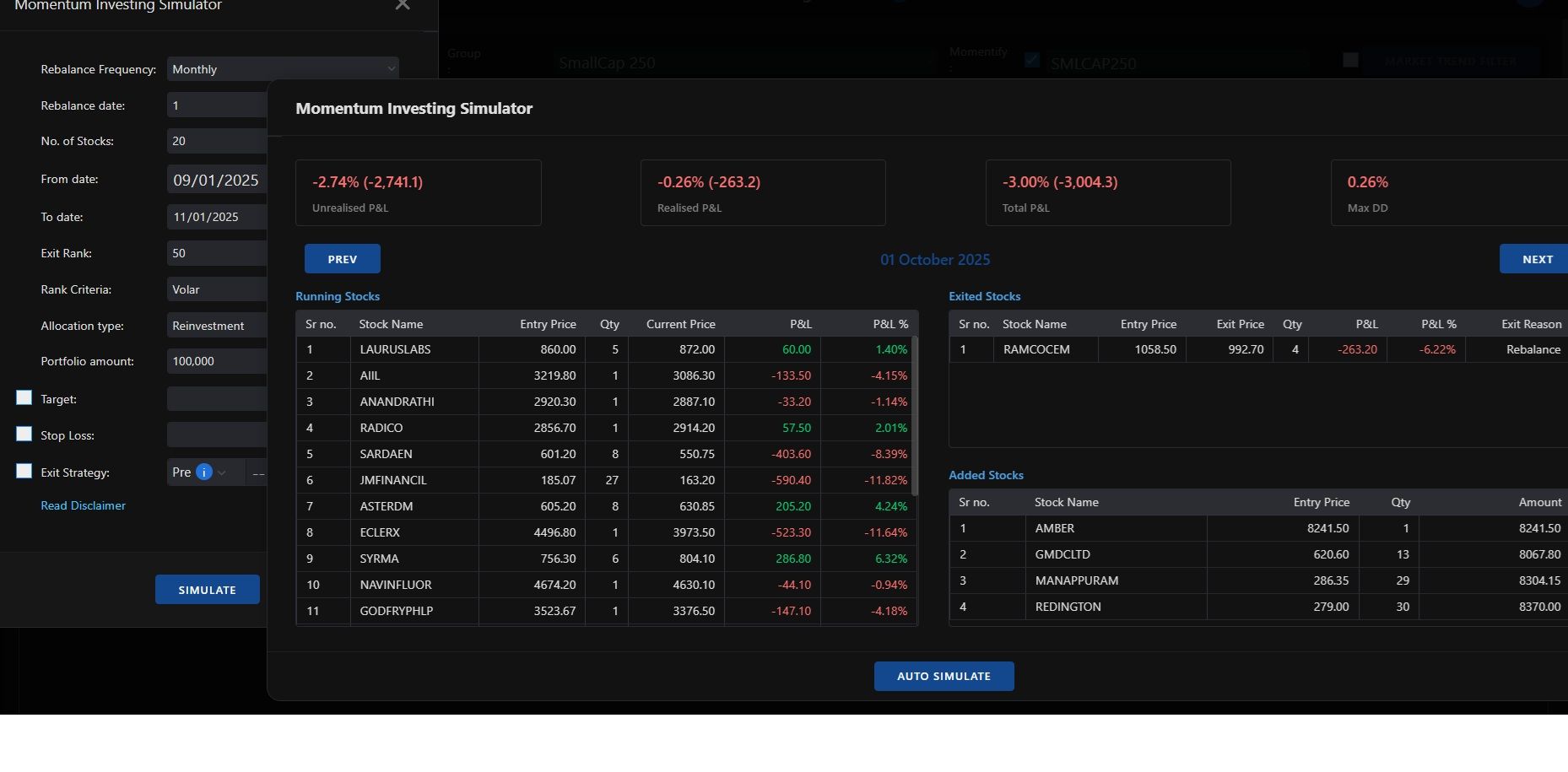

Now, out of curiosity and after reading some feedbacks of users about the wrong backtesting result and discrepancies. I ran the backtesting with same conditions of my real portfolio, same date i.e 01-sep25, it shows 17 stocks ( same result when I started), but next month on 1st-Oct-25, backtesting is showing entry of 4 stocks and exit of 1 stocks , so it makes 17-4+1 = 20 stocks for the month of October whereas in my real portfolio it made me exit 14 stocks and now I am holding only 6 stocks.

Pls look into this, how can we trust the backtesting? what is the point of spending hours with a hope of investing in good strategy through platform? it is really a serious issue, if such issues persist, I am afraid that, users will consider other alternatives available in market.

Hope to hear from you soon and you fix this issue asap.

Attaching backtesting result and real holding for reference.

Thanks & Regards, -

@Definedge @@Definedge-Experts @Prashant shah,

its unfortunate and really disappointing that its been a month and there is not a single acknowledgment from Definedge Team.

What should I do in order to get a reply and get it resolved.

Pls advise. -

I have forwarded the issue to the concern team. Please allow us some time to check and revert.

-

@Brijesh Bhatia Thank you Brijesh Sir,

Regards,

Yogesh Kumar -

Following, Any Update? my first execution date is coming soon.

-

I got a call regarding this but I am not satisfied, they say, in backtesting it takes the Eod data and there might be some difference, to which I replied " yes, some difference, but in backtesting, next month(2nd month) it shows 20 stocks after squaring off some stocks n gave entry to some new one, while executing the real portfolio through momentify, I was left with only 6-7 stocks in my real portfolio and as far as eod data is concerned , momentify also pick stocks as per last day ending price."

So, I am bit confused and unfortunately can't rely on backtesting, it is good on paper, but in reality the story is completely different. The explanations I got , don't satisfy and encourage me to go further until they fix these issues. We are not putting only money, but investing our time and efforts. Thanks & Regards -

Hi,

Momentum investing simulator and Momentify rebalance - both are performing properly.

When you run Momemtum investing simulator for the same period - it calculates EOD data. For example the entry date is 1st. It will consider closing price of 1st for the calculation. While actual execution, Momentify calculates the entry price when you execute the basket. So, there will be a difference in backtested data and the actual execution. Even the number stocks will change. For closer to backtesting, you can execute the basket at around 3 pm on the selected date.I have mentioned this in the book and several times - the backtesting gives us the idea. There will be a difference in the performance while execution. Read this chapter.

https://shelf.definedgesecurities.com/master-momentum-investing-trading-strategies/chapter-10-backtesting/In the long run, the result will be close to the backtesting and it can even be better. There is no reason to doubt the backtesting or Momentum investing because of this. You can always crossoverify the backtesting data with the excel file and Momentify stocks with the strategy fields. You wouldn't find the discrepancy.

Let me know agar abhi bhi doubt hai.

-

@Prashant Shah

Hello,

Prashant sir,I got a call from Definedge and had a gmeet with Mr Rajesh, he patiently listened to my issues and understood what I was trying to convey,he took notes and working on this. Thanks to You for the reply. It helps a lot when issues are addressed properly, it gives us confidence and build trust. I admire Definedge a lot for the its uniqueness and great tools.

Thanks & Regards -

@Prashant-Shah @Brijesh-Bhatia @Definedge

Hello Prashant ji and Brijesh ji,Thanks, I got a call from Definedge and team said that

--> When I initiated the portfolio (01 Sep 25), the system did not consider the Radar conditions that I put, so, it ignored that " Radar Condition" and took 17 stocks ( it should not have taken all the stocks )

-->And when rebalancing date came (01 Oct 25) , it considered " that Radar condition" (because the team did some updates) and some of the stocks, got squared off (the system should not have initiated on 01 Sep 25 itself)

-->Now all the rebalancing is as per my criteria or conditions.

-->I got the answer but again it raises a question about the backtesting, because as per backtesting, one should have 20 stocks but in my real momentify portfolio I am left with 10 stocks (in backtesting, it still ignore that radar condition but in actual portfolio, this issue is solved.)

-->This can create discrepancy in results. Please consider these issues in backtesting.

Thanks to both of you and Definedge Team (Mr Rajesh, he was very patient and attentive) and kudos for your efforts in making this platform unique and great !

Regards,

Yogesh Kumar -

@Yogesh Kumar

I hope definedge team clarifies on this issue.However in my opinion, if in your strategy, you have specified 20 stocks in portfolio, my understanding is that 20 will be the maximum holdings. If there are less than 20 stocks which satisfy all the filter criteria, then your portfolio will feature less holdings.

I've not yet faced this situation, but I guess it can be checked against the Momentum Investing Scanner, at the same time as Momentify Basket is generated - ideally both should be same or similar with minor differences.

-

@G Heble

Hello,I got the answer and satisfied from Definedge Team (why there was a difference in backtesting and real portfolio) and I agree with you as well that ideally both should be more or less same (thts why I raised this query).

My concern is now, if Radar conditions were not updated and the system was not considering Radar conditions in backtesting then there is no point of backtesting with Radar conditions because the backtesting with Radar conditions won't give the true picture.

So, I will make another portfolio through momentify and observe (will not be putting any conditions of Radar, as I can't rely on backtesting with Radar conditions)

Thanks

-

@Yogesh Kumar Hello Yogesh, can we consider radar conditions now ? is it working ? is there any way to check if radar conditions are taking into consideration on the date of rebalancing ?

All these days, till now i am using radar condition in backtesting, I don't see point in backtesting with radar if not taken into consideration? -- your view on this please.

Thanks in advance.

-

@Manigopal Vutla

Hello Manigopal ji,Its working fine, the system is taking the stocks as per Radar condition ( real portfolio ), so I have not squared off the portfolio and infact I will continue with the strategy and will observe it regularly.

As far as backtesting is concerned with Radar conditions, I am hesitant, I will wait at least 6 months and review again my real portfolio with backtesting to see if there is any discrepancy.

I am thinking of deploying 1 more portfolio through momentify but based on only technical conditions.Thanks & Regards

-

@Yogesh Kumar Thanks Yogesh for the information and insights.

-

@Brijesh-Bhatia @Prashant-Shah @Definedge @@Definedge-Experts

Respected Definedge Team, Brijesh Sir and Prashant Sir,

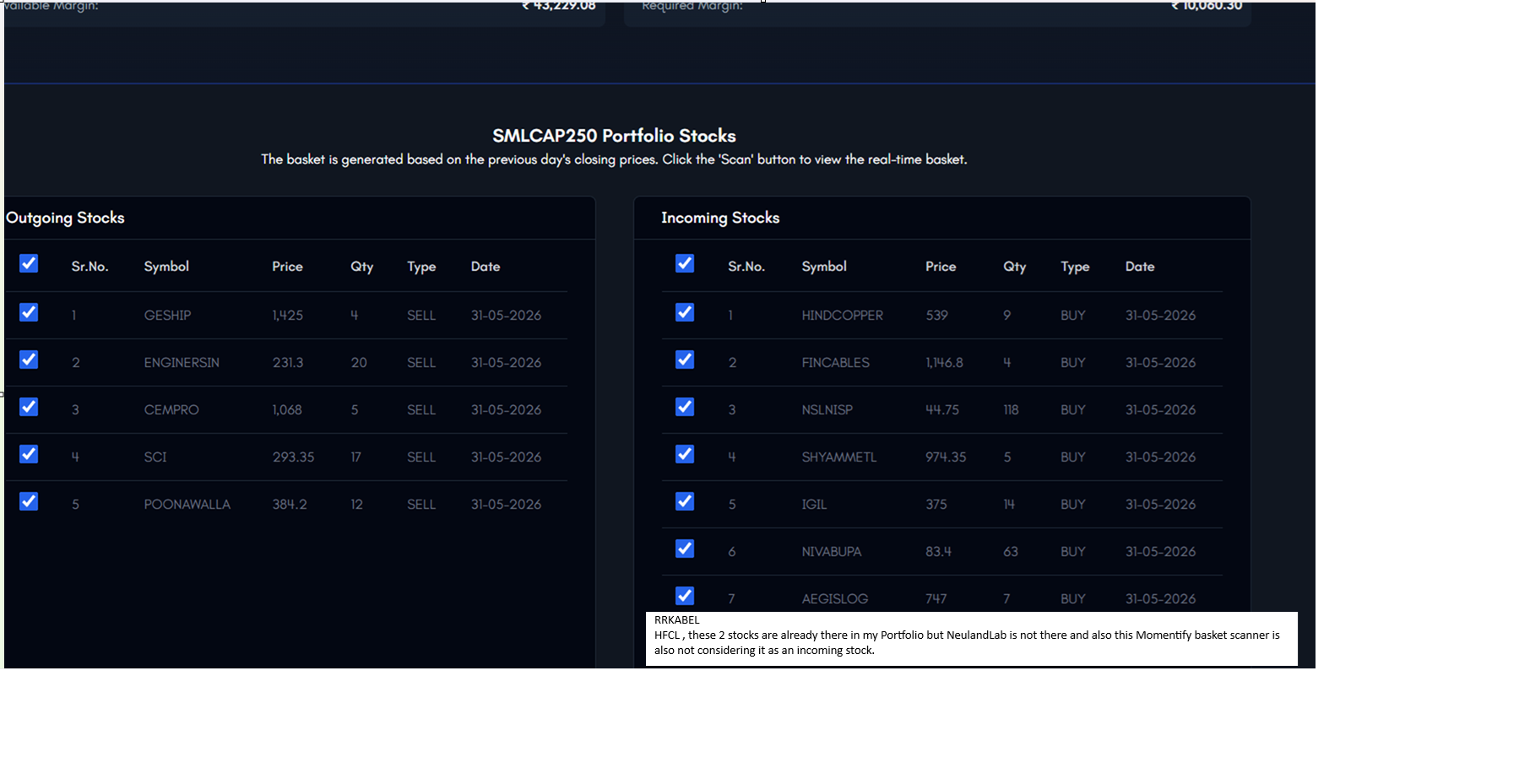

I have been running an investing portfolio through momentify, I had some issues with it in the past and it was resolved, tomorrow is rebalancing date for my portfolio, I did scan and got a basket (as per conditions), so as per basket created by momentify basket scan system some are incoming and some are outgoing.

I did scan the same strategy with

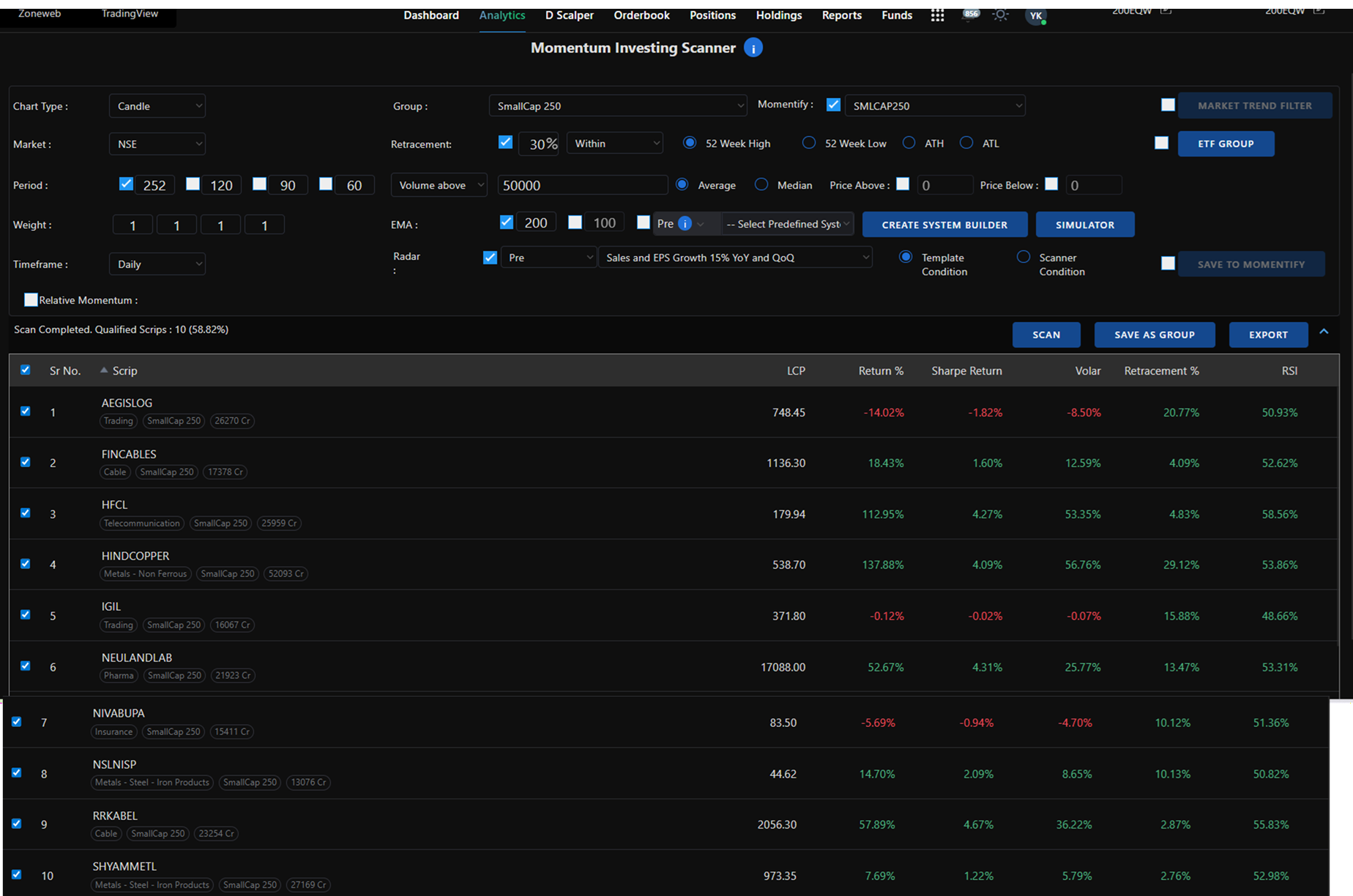

same conditions on Rzone but as per Rzone scanner result, there is 1 more stock which should be incoming but not incoming (in real)as per momentify basket scan system. It means, if we ever do the backtesting in the future, it will include that stock but in real its not considering as an incoming stock (again the question is how much can we rely on backtesting) pls look into this and advice.

same conditions on Rzone but as per Rzone scanner result, there is 1 more stock which should be incoming but not incoming (in real)as per momentify basket scan system. It means, if we ever do the backtesting in the future, it will include that stock but in real its not considering as an incoming stock (again the question is how much can we rely on backtesting) pls look into this and advice.

Thanks & RegardsP.s I am attaching screenshot for your reference and the stock name is "NEULANDAB".

-

Hello sir, As per the screenshots, NEULANDAB met the scanner conditions and appeared in the scan results. However, it was not added to the final momentify basket because the available per-stock allocation was insufficient for its price.

You can verify this in the Momentify logs, where it should show a message indicating insufficient amount. Therefore, the stock was identified correctly but was excluded from the basket due to allocation constraints.

-

@Definedge Thanks For your prompt reply and call, I got the answer after you explained me the default setting and condition.

Thanks & Regards