Serious Issue in Backtest Position Sizing Logic – Inflated CAGR Results

-

Hello @Definedge Team,

I am Definedge user since long time, I was doing momentum trading strategy backtest and found some major issue

While backtesting, I Got 88% CAGR with max DD of 2%, which is ofcouse not possible to achive, thougt to dig down deeper, and I find out that there is issue in QTY logic

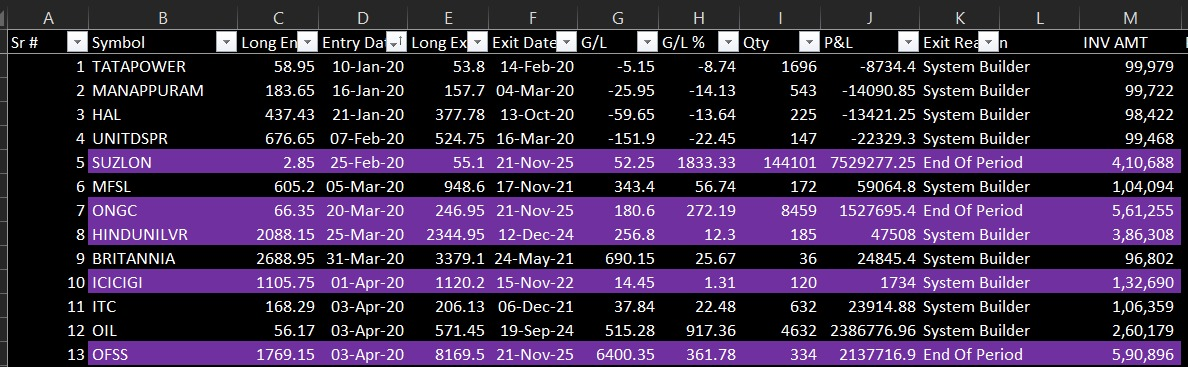

As you can check in pic, colour marked trades has exponential higher qty than what it should be, probably it's due to re-investment approach, but rather than taking price on the date of re-investment, it's simply adding qty in old trade which will be ofcouse at lower rate, so CAGR it shows is too high

I have attached photos here for better clarity

I think it's dangerous reason being,

Backtesting is the foundation of strategic validation. If the platform reports such inflated returns due to incorrect sizing logic:

Users may form unrealistic expectations

Allocate capital based on wrong projections

And potentially incur large financial losses

This is not just a technical bug — it directly impacts decision-making of user and user's trust

I hope this can be addressed quickly, as many users rely on these results to deploy real capital in live markets @@Definedge-Experts

-

@Alpha Trader

I have also brought this issue to their knowledge more than a fortnight ago through email.

I have been advised that they are working on it. -

same issue, every weekend i do backtesting sometimes it don't add up, drop in CAGR and their zone app is slow.

I feel like they are adding new features and not working on issues. waiting patiently, lets see.. -

following

-

I have also raised the concerns regarding backtesting and data's accuracy, moreover, momentify software picked 7-8 stocks but in backtesting for the same time duration, showed different result (20 stocks). Been a month raised this issue but still did not get any reply or resolution. Disappointed...

-

This raise serious concerns, lossing trust day by day and thinking to sqaure off whole portfolio and not to rebuild position untill bugs are fixed

It's ok to have bugs, but it's not fair when user adresse it clealy with proof, but users don't get response from team @Definedge

-

@Alpha-Trader did you get any update ? Thanks in Advance.

-

Not yet, not expecting as well!

-

Hello everyone,

I am looking into it.

There are three types of backtesting in RZone:

Normal Backtesting

Momentum Trading Backtesting

Momentum Investing SimulatorThe above issue raised seems with normal backtesting or momentum trading backtesting - I'll check with the team. I'll get back on the quantity issue raised. I will also have to analyse the conditions used. I'll check the logs.

I myself runs backtesting almost everyday in RZone. Momentum investing simulator is accurate and you can always cross verify with the data. Like @Alpha-Trader did here. I will soon get back on what went wrong here and get it fixed asap.

Sorry for the delay in reply. I will check the Forum on daily basis from now.

-

Hi @Prashant-Shah

Thanks for looking into this. Along with the quantity sizing issue in momentum trading backtests, I also noticed that strategy selection isn't available in momentum backtesting which was earlier available

Requesting you to please address both these points, Happy to share more details if needed

-

I am checking with Rajesh. I'll get back on this.

-

@Alpha Trader Any Update on this thread ?

-

@Prashant-Shah

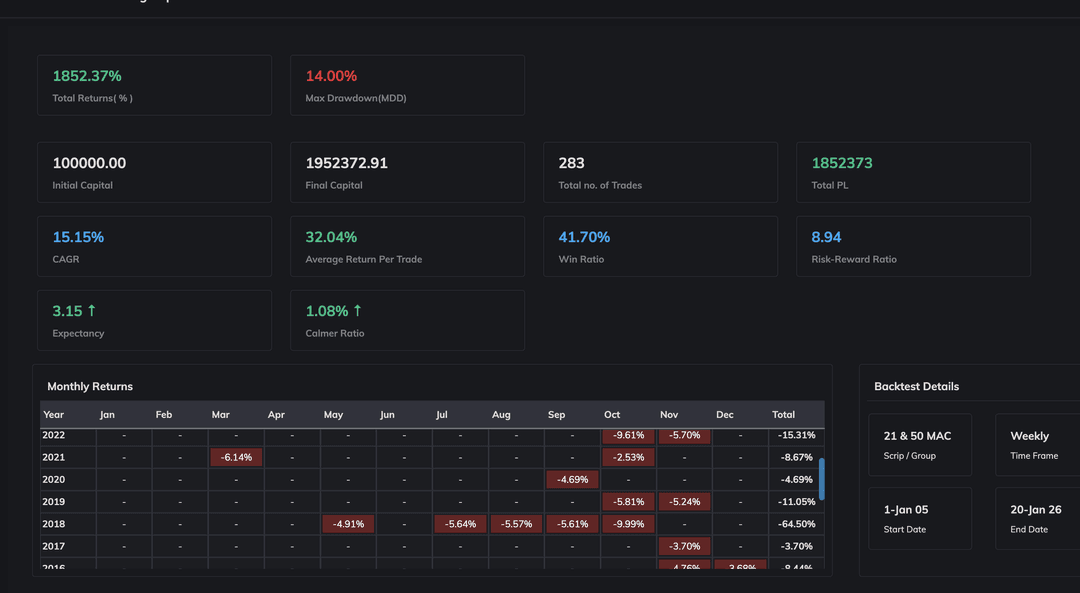

I have also came across issues with momentum trading back testing where the numbers does not add up and seem to be incorrect. ie. Monthly returns table shows negative percentage in all years total however CAGR is positive. CAGR can't be positive if we are getting negative return every year. Please look at the attached image. It's hard to understand which data are correct and which are not?

-

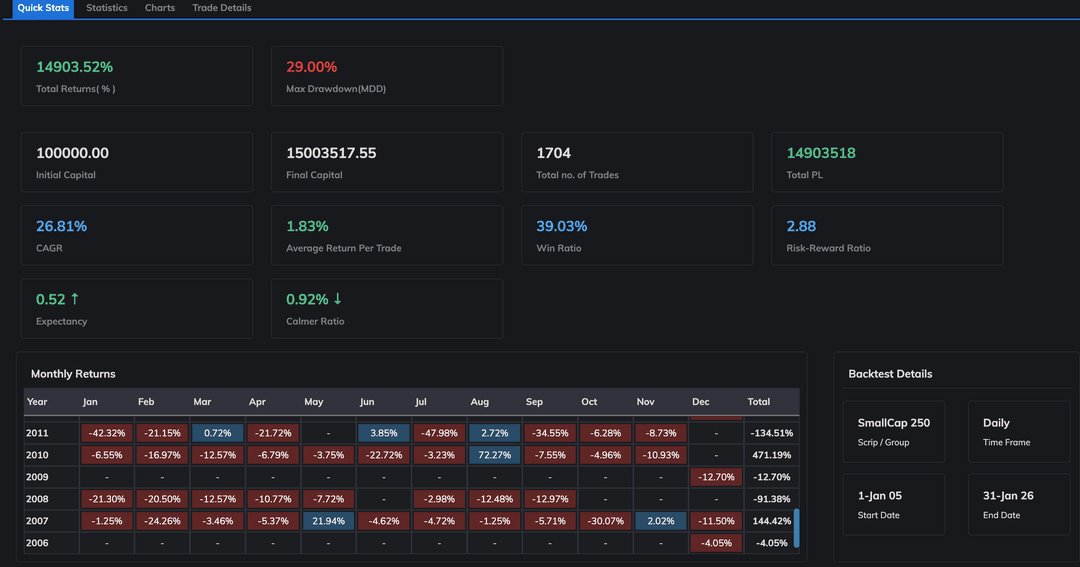

Another example:

Check the year 2010 - All the months in year 2010 have negative returns except Aug and Aug 2010 - the return is +72.27% then how come the total return is 471.19% in 2010? Please find the attached imaged

Still confused about which Options strategy to use in different market conditions?

Still confused about which Options strategy to use in different market conditions?