OK Sir.

Awaiting for receiving the good news from your end.

Vivek Kumar

All Replies

-

-

Dear Team Definedge,

I am a huge fan of your products and a very early fan of Momentify Investing & Trading.

Please accept my request of allowing auto - rebalancing Momentify Investing / Trading portfolio atleast till 3:15PM or even later till 3:20PM to match the closest possible price to EOD.

If there are any regulatory challenges, please let me know, I can do this manually until SEBI listens to us or if there are any technological advancements required, I am damn sure that Definedge can surely do this.

Awaiting your response.Thanking You,

Vivek Kumar

UCC-1267677 -

Hi,

I am unable to register myself for DECMA2026 since yesterday. The Register Now button is not responding and I have tried changing the device / browser but it didn't help.

Please look into it. I have sent a personal message to Prashant Sir as well on his Social Media profile regarding this matter.

Regards,

Vivek Kumar

UCC - 1267677 -

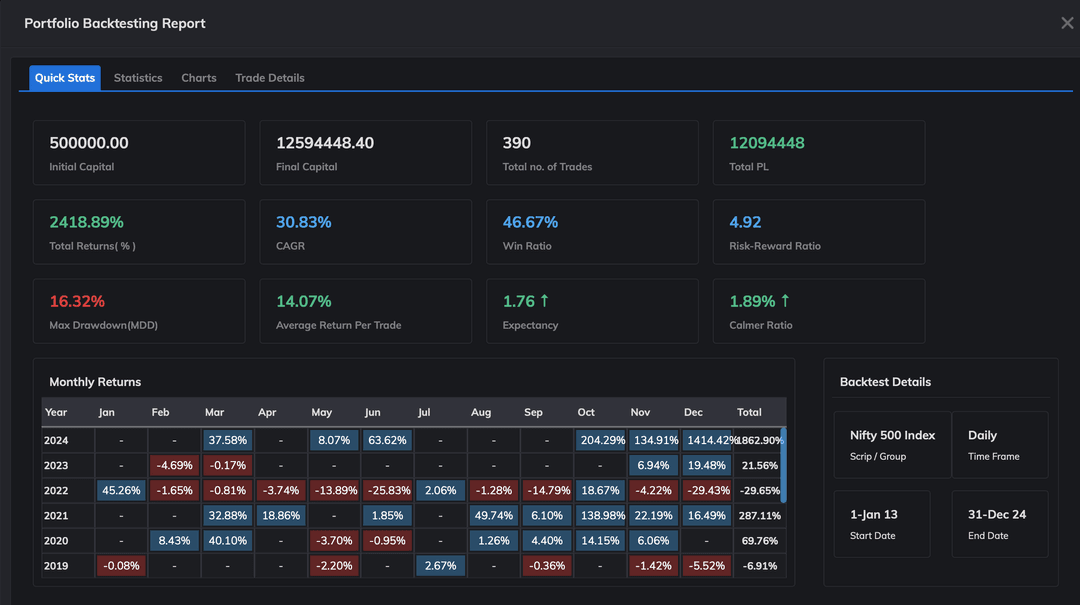

Update on 30th July 2025

Today, the same backtest is showing another CAGR / MDD again.

Screenshot attached.

-

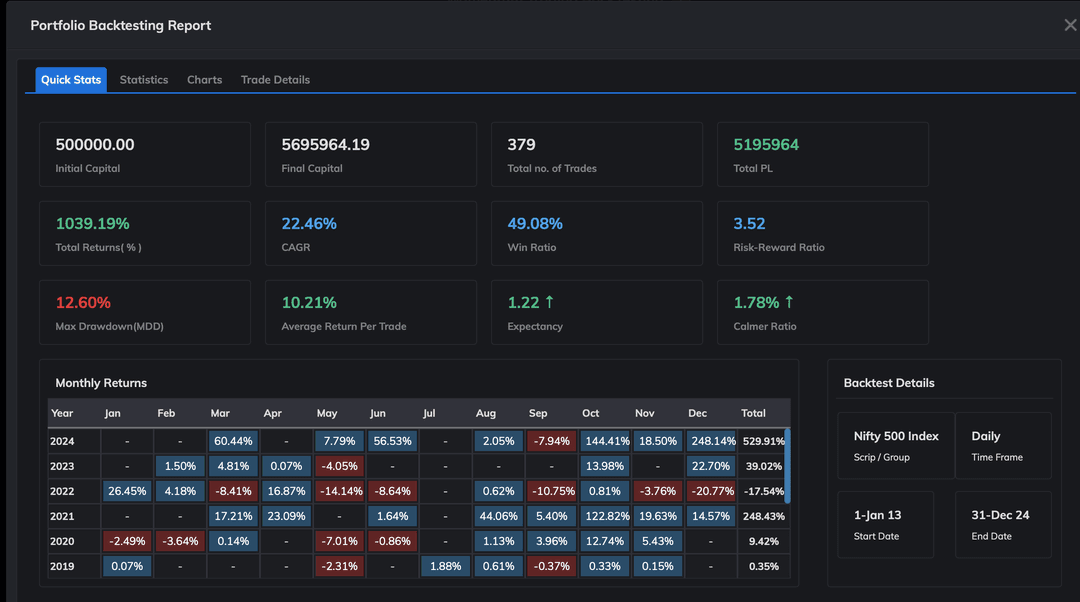

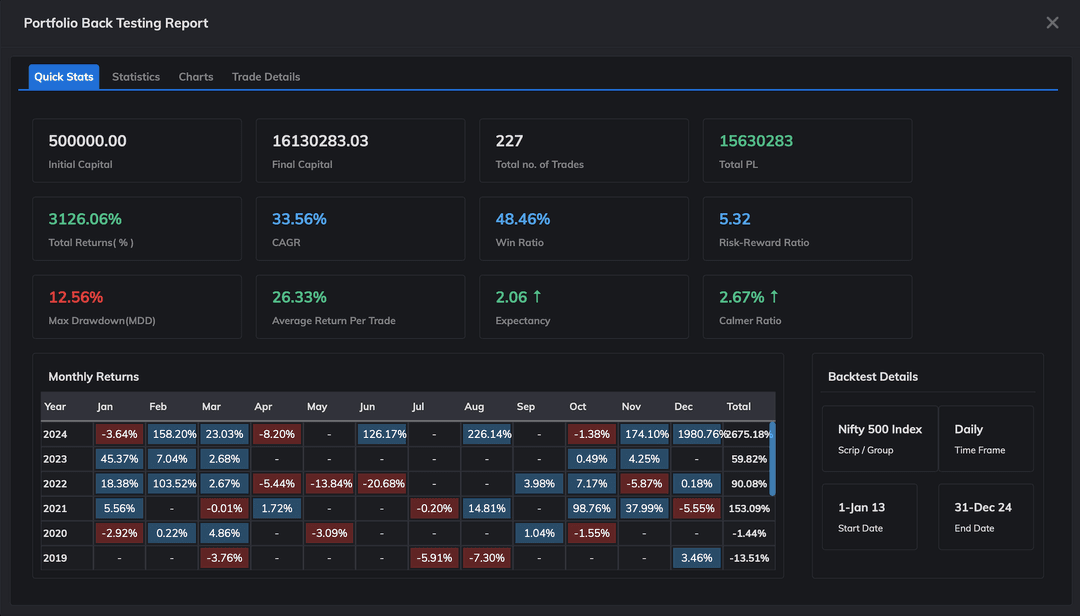

Dear Team Definedge,

I would like to inform you that I have created a Momentum Trading Strategy which is saved to my Momentify platform and whenever I am backtesting this saved strategy in RZONE, it is showing different results on different days despite my "Parameters being equal" each time. To safeguard the manual error, I use the 'Linked to Momentify' tick mark before Backtesting it but the result varies each day.

Example:

Backtesting Period : 2013 - 2024

Stop Loss : 20

Position Size : 15 with 'Reinvestment Option'

Other parameters are saved with Momentify hence 'No chances of manual error' and I always check the parameters manually as well each time.Results:

CAGR / MDD on 18th July 2025: 33.56% / 12.56% (Screenshot attached)

CAGR / MDD on 28th July 2025: 31% / 16% (forgot to take Screenshot)

CAGR / MDD on 29th July 2025: 22.46% / 12.60% (Screenshot attached)The same difference has been observed while backtesting another data sample from 2001 - 2012.

-

Thankyou so much Sir for arranging callback. Hope, will get the call today.

-

Dear Team Definedge,

I backtested a multi timeframe based Renko strategy via Momentum Trading option and have observed that the Exits were rightly at the time when it was closing below D-smart (Below D-Smart option available under 'Popular' in Backtesting Engine) but my Entry condition was Swing Breakout Pattern however I have observed that if New Brick has formed on 1st January 2024, marking a new Swing High pattern, the trades are being taken on 2nd January 2024 and such incidents have occurred multiple times as per the exported trades result.

Please arrange a callback at my registered number to elaborate this issue and necessary resolution by your end.Thanking You,

Vivek Kumar

UCC - 1267677 -

Dear Definedge Team,

When we backtest any trading system in RZONE via Momentify linked trading system then usually we place our Rebalance Date as 1st of each month. I have observed that trades executed in backtesting are executed at Closing Price as on 1st of that particular month. So shall I assume that the System is ranking Stocks as on last day of the Month itself and executing trades on 1st of each month to match with our real life scenario where we will be receiving notification in the morning itself on 1st of each month as the System must have ranked Stocks as on last day of the month for providing us the notification next day?

Please guide me whether my understanding is correct or not. -

Dear Sir,

I do not know why but Chat option was not enabled for me, I even tried using other devices.

Please clarify the below mentioned points w.r.t. MIP

Question 1. As backtest is based on Buying and Selling at Closing Price which is not that practical in real life. So what methodology do you suggest to keep our Buying Price as much as possibiel nearer to Closing Price.

2. If I want to buy LIQUIDBEES when Market is not that much moving and how will that automatically get replaced by Stocks during next rebalancing

3. Stop Loss are getting hit on closing basis. Any suggestions to mimic the Closing Price at best possible wayVivek Kumar

UCC - 1267677 -

Dear Team,

I have backtested one strategy to deploy in Momentify this month with 15% Stop Loss (defined in Momentify itself) but while checking trades on random basis, I have observed in the below mentioned trade has technically hit its Stop Loss but was not triggered by the system and had continued the trade.

(Screenshot attached - GodrejInd)

-

@@Definedge-Experts

Please guide. -

I am new to Definedge ecosystem and was backtesting MIP37 after reading Prashant Sir's book with modified parameters but I observed that when I changed the Market Filter from only Nifty 500 to Relative Strength based Market Filter (against Nifty GS Composite) with my preferred Stop Loss the result was improved, let's say, "X% Max Drawdown with Y% CAGR" however when I changed it back to MIP37's default Market Trend Filter i.e. Nifty 500 with D-Smart the results were different viz. "A% Max DD with B% CAGR". The period for the In Sample backtest was 01-01-2001 to 31-12-2008 in both the cases.

My question is that when there is 'No Data for Nifty GS Composite during this period' then what calculation is being done at the backtest which has improved the results when using Market Trend Filter as RS with Nifty GS Composite.

Suggestion / Feedback : Momentify Auto-rebalane @ 3:15PM or later to match near EOD Price

Suggestion / Feedback : Momentify Auto-rebalane @ 3:15PM or later to match near EOD Price

DECMA2026

Unstable Momentum Trading Backtesting Results - Renko Charts

Unstable Momentum Trading Backtesting Results - Renko Charts

Momentum Trading - Renko Multi timeframe Issue - UCC 1267677

Momentum Trading - Renko Multi timeframe Issue - UCC 1267677

Momentify Rebalancing Date & Date of Execution

Questions - Momentify Webinar

Stop Loss not triggered in RZONE linked to Momentify during Backtesting

Query: Improved Backtesting Results in MIP37 without sufficient GS Composite Data

Query: Improved Backtesting Results in MIP37 without sufficient GS Composite Data