Vriddhi Strategy {Long Only}

-

The primary objective of the Vriddhi strategy is to identify and capitalize on bullish opportunities in the stock market. The strategy focuses on stocks in a bullish trend by meeting two critical criteria: being above their long-term 200-Day Exponential Moving Average (200DEMA) and signalling bullish momentum through a positive crossover of the Adaptive Relative Strength Index (ARSI).

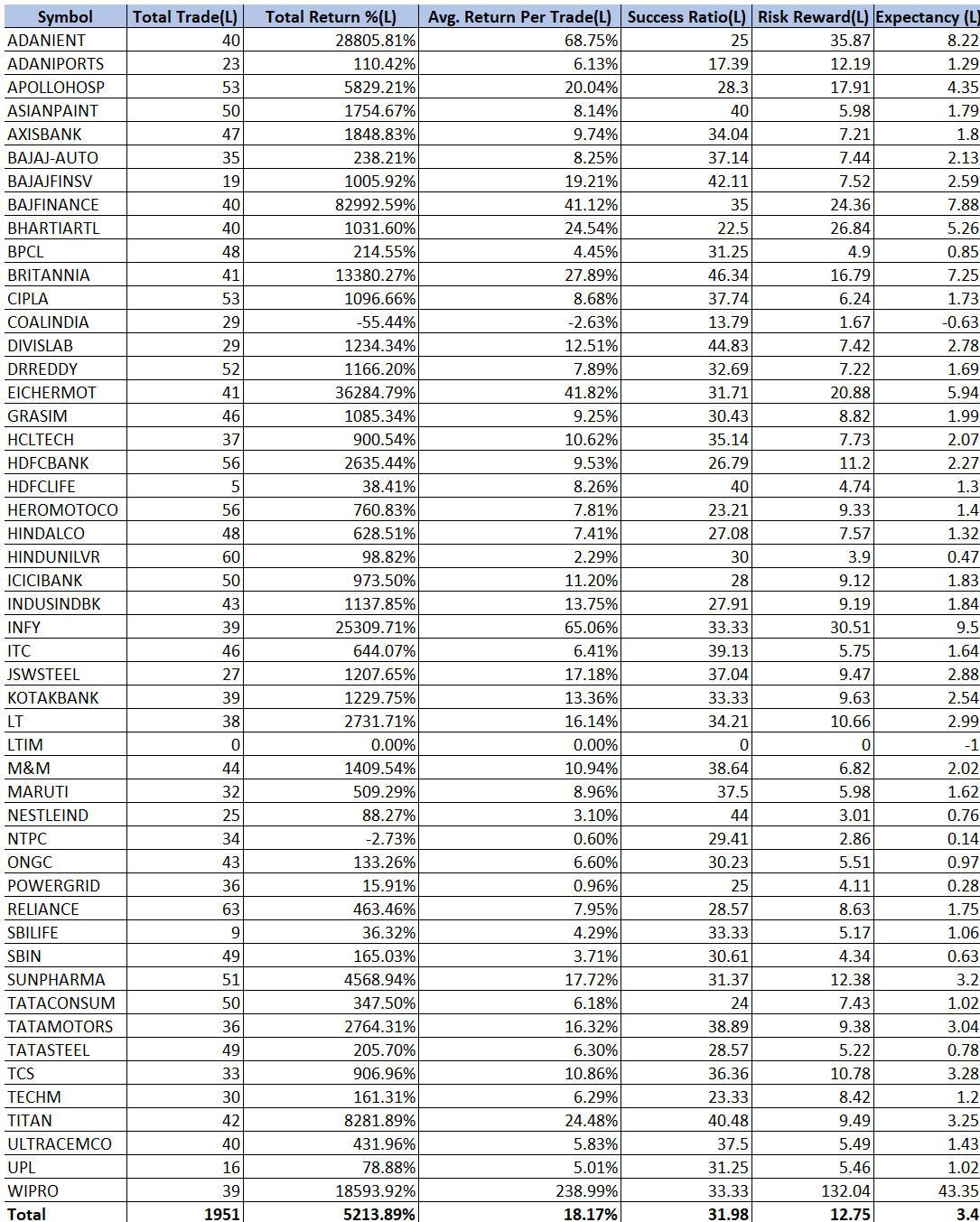

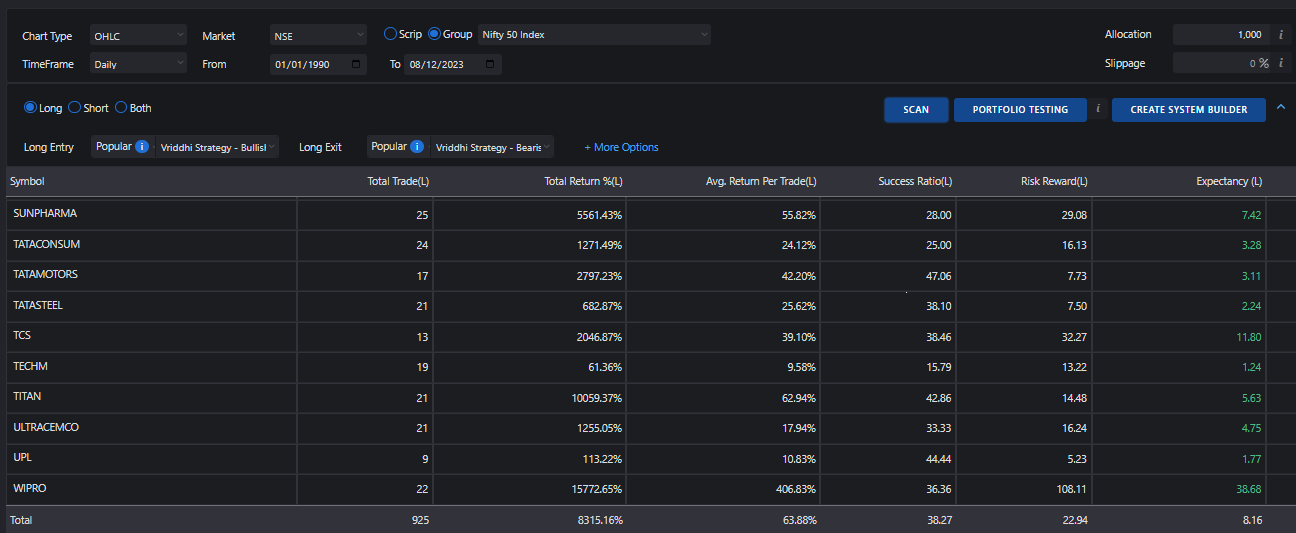

Here is the backtesting result on the current Nifty50 stocks:

Source: Definedge ScannerThis scanner will be available soon to existing Definedge Securities users.

-

Is there a video for the s strategy ?

-

@Somen Sangani Not yet.

-

any specific reason for choosing N50 universe? also whats the exit criteria?

-

Nifty50 was just an example to highlight. You can select any group or your group.

We have an inbuilt scanner for Entry and Exit in RZone Scanners, you can explore it.

-

I got different result when I do the backtest. Please help to check it out Sir

-

@Sugapriya Thimma As the data date changes, the back testing results will change for any strategy.

-

Sir Can you please explain the various results obtained in back testing. What value ranges are called good results in back testing in risk reward and expectancy. Alternatively what all parameters are of utmost importance to be seen while analysing the backtested results as the same in not mentioned anywhere. I am a new user at Dwfinedge with customer ID 1246020, Kindly advise

-

@OMESH YADAV

Risk-Reward Ratio is a measure of the potential profit compared to the potential loss in a trade. It is calculated by dividing the potential reward (profit) by the potential risk (loss). Anything above 2 is considered good.Expectancy is a measure of the average amount of profit or loss that can be expected per unit of risk over a series of trades. A positive value implies that, on average, each trade contributes positively to the account balance. The higher the positive expectancy, the better.

-

Thanks Sir for clarification. I have designed a system and backtested on Nifty 650 Wef 1990 with entry and exit inputs. The results are Total Trades (20.9), Total % profitable (77), Avg Return per trade (3.69) Risk Reward( 1.7) Success Ration (81.43) Expectancy (1.2). As per your clarification the system seems to be good to me. Am I correct in my analysis or do I need to look into it further. Request assist

-

The same system when run on bullish momentum stocks of Define edge has produced results as Total Trades (30.37), Total % profitable (106.23), Avg Return per trade (3.5) Risk Reward( 2.18) Success Ratio (80.14) Expectancy (1.55).