Hello @Definedge,

Kindly provide option to rebalnce fortnightly, it will be much of a help and also sweet mid point between weekly and monthly rebalancing option

Thanks

Pro User

Hello @Definedge,

Kindly provide option to rebalnce fortnightly, it will be much of a help and also sweet mid point between weekly and monthly rebalancing option

Thanks

@Prashant Shah Nifty 500 is also not historically adjusted?

Hi @Prashant-Shah

Thanks for looking into this. Along with the quantity sizing issue in momentum trading backtests, I also noticed that strategy selection isn't available in momentum backtesting which was earlier available

Requesting you to please address both these points, Happy to share more details if needed

Not yet, not expecting as well!

F&O group is not historically adjusted, note this thing, if you're not aware about

This raise serious concerns, lossing trust day by day and thinking to sqaure off whole portfolio and not to rebuild position untill bugs are fixed

It's ok to have bugs, but it's not fair when user adresse it clealy with proof, but users don't get response from team @Definedge

If stock goes below EMA, it should exit as per the condition given, in Momentify it got exited, but in RZON MIP shows stock is still in portfolio

I have checked chart and shared pic, it should have been actully exited, which means Rzon backtesting results are not accurate

When I have explored this platform, I was quite impressed, but as days passes more and more bugs I am finding and reporting to team but getting no respose!!!!

@Raju-Ranjan @@Definedge-Experts Kindly do the needful ASAP

Hello @Definedge Team,

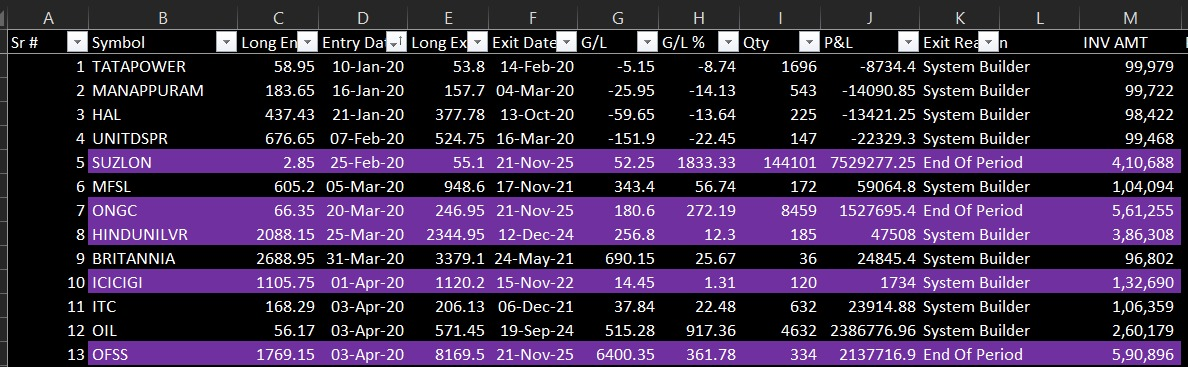

I am Definedge user since long time, I was doing momentum trading strategy backtest and found some major issue

While backtesting, I Got 88% CAGR with max DD of 2%, which is ofcouse not possible to achive, thougt to dig down deeper, and I find out that there is issue in QTY logic

As you can check in pic, colour marked trades has exponential higher qty than what it should be, probably it's due to re-investment approach, but rather than taking price on the date of re-investment, it's simply adding qty in old trade which will be ofcouse at lower rate, so CAGR it shows is too high

I have attached photos here for better clarity

I think it's dangerous reason being,

Backtesting is the foundation of strategic validation. If the platform reports such inflated returns due to incorrect sizing logic:

Users may form unrealistic expectations

Allocate capital based on wrong projections

And potentially incur large financial losses

This is not just a technical bug — it directly impacts decision-making of user and user's trust

I hope this can be addressed quickly, as many users rely on these results to deploy real capital in live markets @@Definedge-Experts

This happens due to split,bonus and other corporate actions, if you see for longer horizon it won't affect much

recently I bought 9 shares as per system, but after split, I done backtesting and it showed 10 shares

so minor differnce could be there, but in long run it average out

Same thing happned with me as well, much relatable and pls @Definedge team consider this suggestion

Dear @Definedge team,

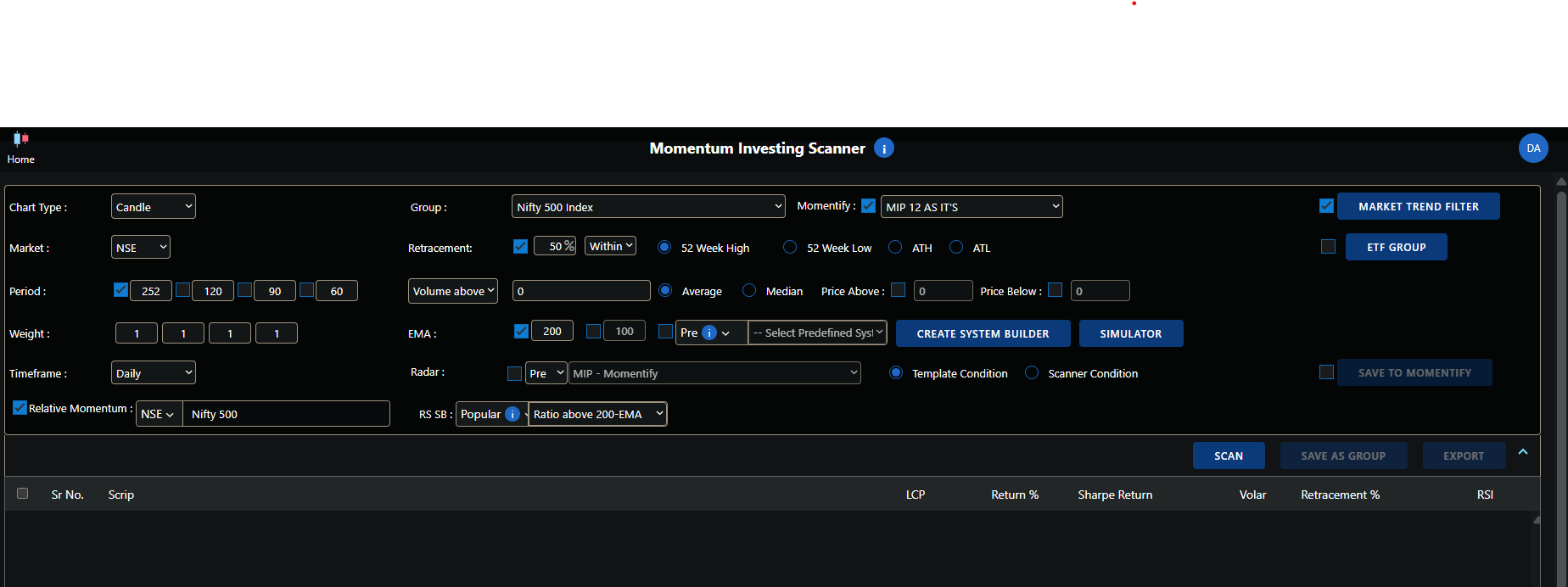

Currently, the Momentum Investing section in Definedge provides a Scanner / Template Condition tab, which helps a lot to directly check the strategies applied ,This feature is extremely useful for stock analysis and time saver

However, the Momentum Trading section does not have a similar tab, kindly provide it as early as possible

Thanks

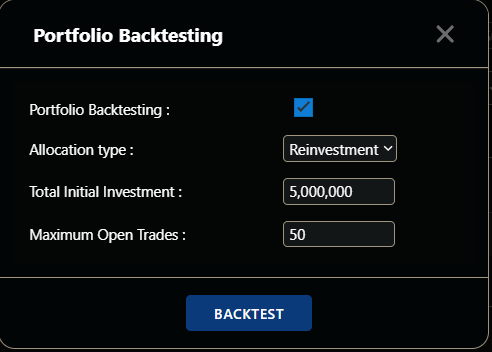

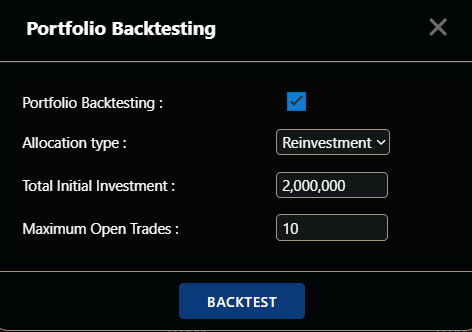

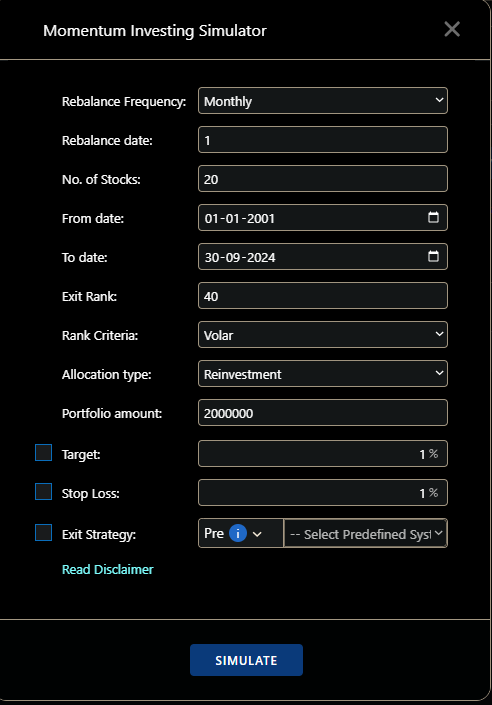

In any startgy if you are selecting allocation: reinvestment

After a 5 year capial could be 60L, and position will be taken according to 60L, but SL calculation will be on base capital 20L, which is wrong and doen't give right results

SL amount: Buy rate x qty x SL %

if price closes below SL amount, stock should be exited

Dear team, @Definedge @@Definedge-Experts

I’ve been using the momentum trading feature and noticed that the Max SL (Stop Loss) parameter doesn’t seem to be functioning as expected.

After investigating further, I found that the system currently calculates the Max SL based on the base capital, whereas it ideally should be calculated based on the amount invested in a particular stock AFTER REINVESTEMENT

so capital should be updated after each trade but it's not, which seems minor bug and hence max sl is not working which can be serious issue if not resolved user can mis interprete data and start trading, so kidnly do the needful ASAP

Thanks!

This was really helpful, thanks Prashant sir

Hi Team @Definedge @@Definedge-Experts

I’ve been analyzing trade results generated from one of the backtesting systems and wanted to confirm is survivorship bias accounted for in the data feed used by RZONE?

Could you please clarify whether the historical database used in Definedge backtests includes delisted or suspended stocks, or it only contains currently listed symbols?

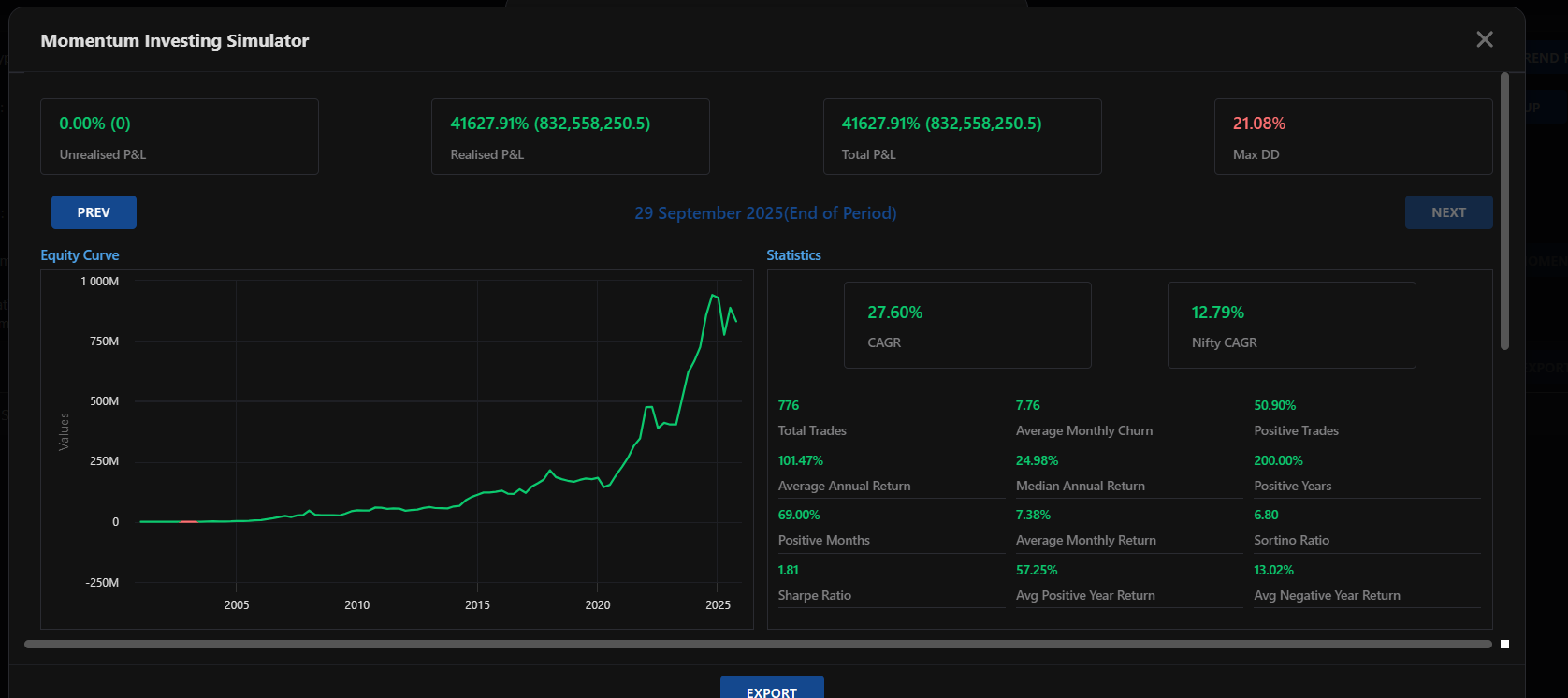

200% positive years is not possibe, i have checked calcaultions here are the differences

CAGR: ~28.58% (vs site 27.60%)

Average Annual Return: ~34.69% (vs site ~101.47% )

Median Annual Return: ~24.12% (vs site ~24.98%)

Positive Years: ~87.5% (vs site 200%)

Dear Definedge Team,

While using RZone, I noticed that the backtest stops completely if there is even a momentary internet drop (ping loss for a second). This forces the user to restart the entire backtest from the beginning, which is time-consuming and frustrating, especially for longer backtests

Suggestion:

It would be very helpful if RZone could:

Auto-resume backtesting from the point where it stopped once the internet reconnects, instead of restarting from 0.

Provide a “resume from last checkpoint” option so users don’t lose progress due to a temporary disconnection

Thanks

I have copied MIP 12 and backtested as it's but results are not matching with what mentioned in book

Is there any way to get rolling return calculation of backtesting , in definedge platform? or do we need to export in excel and have to calcute there by ourselves ?

I have taken MIP 35 strategy as it's from sample strategy given in momentify platform, and kept all setting same as it's

but results are varing massively on what I got on platform vs what shown in book

Also it will help a lot if you add time it took to recover from drawdown

There must be confirmation popup message when closing backtest results, after waiting for 10-15 minutes for backtest, results appears and if close button pressed by mistake it immdetely closing results, now user have to run those backtest again, and it also takes computing power for you which is unnecessary, kindly do the needful, I have expereinced it multiple times so might be happening with many others as well

Just got book delivered, and reading it non stop, feels like getting years of wisdom and knowledge in hours, thanks @Prashant-Shah for making it possible

Hi Team,

I’m writing to recommend adding Max Drawdown (Total P&L/NAV), to the performance dashboard, alongside the realised‑only Max DD currently shown. This captures the largest peak‑to‑trough fall in portfolio equity after mark‑to‑market and aligns with how professional reports evaluate downside risk.

I belive it's necessary reason being,

Industry reporting computes drawdowns from NAV/equity, which includes unrealised gains and losses via mark‑to‑market, so excluding them understates max risk which portfolio may face and investor/trader maybe not mentally prepare for this

I hope request will be considered

Thanks